When Can a Credit Card Company Sue You? Know Your Rights

Credit card debt can move from manageable to stressful when payments fall behind. Once accounts remain unpaid for a longer stretch, the possibility of legal action starts to enter the picture. Still, lawsuits do not happen right away.

Credit card companies usually follow a long collection process before stepping into court. Understanding this timeline helps reduce panic and gives room to act early with realistic solutions.

Credit card issuers often prefer resolution outside court because litigation costs money and time. Even when balances remain unpaid, communication and negotiation options usually exist long before any lawsuit appears.

Can a Credit Card Company Sue for Unpaid Debt?

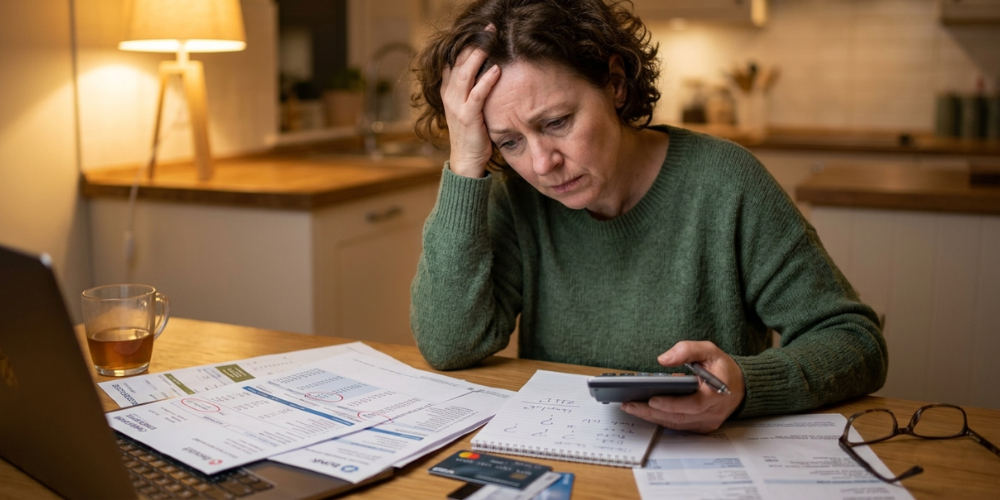

A credit card company can legally sue for unpaid balances. Data from the Consumer Financial Protection Bureau (CFPB) shows creditors file lawsuits in about 12% of cases, with an average debt amount near $2,700. This figure is only an average, meaning cases can involve smaller or much larger balances depending on the situation.

Freepik | Consistent communication prevents credit card companies from filing a debt recovery suit.

Several factors influence whether a lawsuit becomes likely:

1. Communication behavior – Creditors track how consistently contact is maintained. Ignoring calls or written notices may increase the chance of escalation. Open communication often keeps accounts within negotiation territory.

2. Outstanding balance size – Higher balances may trigger more aggressive recovery efforts since financial recovery potential is greater.

3. Payment delay length – The longer an account remains unpaid, the more serious the collection stage becomes. Lawsuits are rarely the first step.

4. Financial indicators – Credit reports and banking patterns can signal whether repayment seems possible. Steady income or active accounts may increase perceived recoverability.

5. State regulations – Some states place restrictions on debt lawsuits, especially involving debt buyers. For example, several states limit small claims court use or require strict documentation before filing. These rules are designed to reduce weak or incomplete lawsuits.

Even with these conditions, lawsuits remain a last-stage tool for most issuers.

Timeline Before a Credit Card Lawsuit Happens

Credit card accounts usually pass through multiple stages before reaching legal action. Each stage reflects increasing seriousness in delinquency.

Around 30 days late

A missed payment triggers late fees. The account becomes officially overdue. Reminder emails or alerts often begin at this stage.

60 to 90 days late

Collection activity increases. Calls, emails, and letters become frequent. Credit reporting agencies are notified, which may reduce credit scores. Card usage may also be restricted.

120 days late

Accounts often move to internal collections or are sold to third-party collection agencies. Credit damage deepens, and recovery efforts intensify.

180 days late (about six months)

This stage is often considered default. Many issuers charge off the debt for accounting purposes. Legal action becomes more likely, either through the original creditor or a debt buyer.

This timeline shows that lawsuits typically appear after months of missed payments, not immediately after a single missed due date.

What Happens When Payments Stop

Before any lawsuit is considered, several financial and credit-related actions usually take place.

Credit card companies usually respond to missed payments with a series of escalating actions. Late fees are applied soon after a payment is missed, and delinquency is typically reported to credit bureaus after about 30 days.

If the account remains unpaid, interest rates may rise around the 60-day mark. Credit limits can also be reduced or accounts closed entirely. Alongside these steps, repeated contact through calls, emails, and written notices continues in an effort to recover the balance.

Credit damage increases with time, especially when accounts remain unpaid beyond 90 days. Open communication can change the outcome at this stage. Creditors often consider modified repayment plans, reduced payments, or temporary relief options when hardship is explained clearly.

What a Charge-Off Really Means

Freepik | Despite being labeled a “loss” by banks, a charged-off account remains a valid financial obligation.

A charge-off usually occurs after 120 to 180 days of nonpayment. This term often causes confusion.

A charge-off does not cancel the debt. Instead, it means the creditor has written it off as a loss for accounting purposes. The obligation to pay still remains valid.

After a charge-off, the debt doesn’t disappear. The original creditor may still pursue collection efforts, the account can be handed over to a collection agency, or it may be sold to a debt buyer who then takes over the recovery process.

Debt buyers purchase accounts at reduced prices and pursue collection independently. These entities may also file lawsuits if repayment does not occur.

Debt Collectors and Lawsuits

Debt collectors and debt buyers can also take legal action. In some cases, they pursue lawsuits more actively than original creditors because their business model depends on recovery.

When a debt collector makes contact, verification becomes a key step. A written request can help confirm whether the debt truly belongs to the individual, whether the stated balance is accurate, and whether the collector has the legal authority to pursue and collect the debt.

Statutes of limitations also matter. These laws vary by state and set deadlines on how long legal action can be filed. Once expired, lawsuits may no longer be enforceable, though collection attempts may still occur.

Debt situations with collectors generally lead to four possible outcomes:

1. Payment in full

2. Negotiated settlement

3. Disputed claim

4. No response (high risk approach)

Communication often prevents escalation, especially when repayment arrangements are realistic.

What Happens After a Credit Card Lawsuit Is Filed

Once a lawsuit begins, official court documents are issued. Ignoring them creates serious consequences.

If no response is filed, the court may issue a default judgment. This gives the creditor or collector the right to take stronger recovery steps such as garnishing wages, accessing or freezing bank accounts, and placing liens on certain assets, depending on state laws.

Responding to the lawsuit is critical. Courts typically provide a limited timeframe, often around three weeks, to submit a formal answer.

The process typically starts with carefully reviewing the summons and noting all legal instructions. Deadlines must be checked right away to avoid missing the response window. A written answer is then prepared and submitted to the court within the required timeframe. If the case moves forward, attendance at scheduled hearings becomes necessary to present the response.

Defenses may include identity errors, incorrect balances, or expired statute of limitations. Legal guidance can improve outcomes, especially when documentation is complex.

Legal Support and Representation

Representation is not required but can influence results. Studies from the Pew Research Center suggest individuals with legal support are more likely to settle or succeed in disputes.

Options include:

1. Private attorneys specializing in debt defense

2. Legal aid organizations offering free assistance

3. Self-representation in small claims court

Cost often becomes a deciding factor, but even limited legal guidance can help clarify rights and responsibilities.

Handling Debt Before It Reaches Court

Freepik | Settle your debt through affordable monthly installments to keep the matter out of court.

Preventing escalation remains possible in many cases. Credit card companies often accept negotiated solutions before pursuing lawsuits. Common approaches include:

1. Payment plans

Structured monthly payments based on affordability.

2. Lump-sum settlements

Reduced payoff amounts in exchange for closing the account.

3. Debt management programs

Structured plans handled through credit counseling services.

4. Temporary relief arrangements

Short-term reductions or skipped payments during financial hardship.

Successful negotiation usually depends on early communication. Once agreements are reached, written confirmation protects both sides.

What Credit Score Impact Looks Like

Credit reporting damage begins long before court involvement. Missed payments remain on credit reports for up to seven years from the original delinquency date.

Even though judgments themselves do not directly appear on credit reports, financial consequences can indirectly affect credit health. Wage garnishment or reduced income may lead to additional missed payments on other accounts.

Long-term delinquency has a stronger impact on credit scores than the lawsuit itself.

Credit card lawsuits typically follow months of missed payments rather than sudden action. Accounts usually move through structured stages, starting with late fees and ending in charge-off or collection transfer before legal steps are considered.

Communication, early negotiation, and awareness of timelines play a major role in avoiding court involvement. Once a lawsuit is filed, response time becomes critical to prevent default judgment and further financial consequences.

More in Legal Advice

-

Brooklyn Beckham’s Billionaire Father-in-Law Breaks Silence on the Family Feud

Brooklyn Beckham’s Billionaire Father-in-Law Breaks Silence on the Family FeudThe Beckham family drama just took another sharp turn. This time, the voice cutting through the noise belongs to billionaire investor...

February 22, 2026 -

Notre Dame Faces Faculty Resigns After Controversial Appointment

Notre Dame Faces Faculty Resigns After Controversial AppointmentTension is rising at the University of Notre Dame after two scholars cut formal ties with the Liu Institute for Asia...

February 22, 2026 -

High Court Upholds Malay Celeb Preacher Da’i Syed’s Rape Conviction

High Court Upholds Malay Celeb Preacher Da’i Syed’s Rape ConvictionThe Shah Alam High Court has spoken, and it spoke clearly. Celebrity preacher Da’i Syed will go to prison now, not...

February 15, 2026 -

Venezuela Opens Oil Industry as U.S. Threatens Cuba Tariffs

Venezuela Opens Oil Industry as U.S. Threatens Cuba TariffsVenezuela has passed a significant law change aimed at opening its oil industry to foreign investment. The move, endorsed by acting...

February 15, 2026 -

Is a ChatGPT-Written Will Legal?

Is a ChatGPT-Written Will Legal?At first glance, using AI to draft a will seems like a smart idea. It’s fast, free, and has a modern...

February 6, 2026 -

Prince Harry Supports Elizabeth Hurley in Tabloid Privacy Case

Prince Harry Supports Elizabeth Hurley in Tabloid Privacy CaseLondon’s High Court became the center of attention as Prince Harry appeared in support of Elizabeth Hurley during an emotional hearing...

February 6, 2026 -

5 Ways AI Is Transforming Daily Legal Workflows

5 Ways AI Is Transforming Daily Legal WorkflowsAI did not storm into law firms with fireworks. It slipped in through contracts, research tabs, inboxes, and meeting notes. By...

February 1, 2026 -

How to Legally Protect Your Side Hustle Without Spending a Fortune

How to Legally Protect Your Side Hustle Without Spending a FortuneStarting a side hustle is a practical way to test a business idea, generate extra income, or lay the foundation for...

February 1, 2026 -

Mayor Zohran Mamdani Appoints Christine Clarke as Human Rights Chair

Mayor Zohran Mamdani Appoints Christine Clarke as Human Rights ChairOn January 7, 2026, during his first full week in office, Zohran Mamdani made a move that set the tone for...

January 25, 2026

More From Lawyers Favorite

-

Criminal AttorneyUS Supreme Court Limits Sentence Reductions for Federal Prisoners

Criminal AttorneyUS Supreme Court Limits Sentence Reductions for Federal PrisonersThe U.S. Supreme Court has issued a major ruling that reshapes how far prison reform laws can reach into past sentencing....

June 12, 2026 -

Celeb JusticeInside Ex-Prince Andrew’s “Bleak” Life in Exile as New Claims Emerge

Celeb JusticeInside Ex-Prince Andrew’s “Bleak” Life in Exile as New Claims EmergeOnce positioned near the center of Britain’s royal institution, Andrew Mountbatten-Windsor now faces a reality far removed from palace ceremonies and...

June 6, 2026 -

Legal AdviceU.S. Lawmakers Push Bill to Expand Burn Pit Benefits to Civilian Workers

Legal AdviceU.S. Lawmakers Push Bill to Expand Burn Pit Benefits to Civilian WorkersA bipartisan group of U.S. lawmakers has introduced a draft proposal aimed at expanding workers’ compensation access for civilian federal employees...

May 30, 2026 -

Law DegreePentagon AI Use in War Raises Questions on Legal Limits and Accountability

Law DegreePentagon AI Use in War Raises Questions on Legal Limits and AccountabilityAI has moved from support tools in defense operations to a central part of how modern warfare is conducted. In the...

May 22, 2026 -

Criminal AttorneyIdaho Bathroom Law Faces Federal Lawsuit by Transgender Residents

Criminal AttorneyIdaho Bathroom Law Faces Federal Lawsuit by Transgender ResidentsA new Idaho law restricting restroom access has triggered a federal court challenge from transgender residents who say it places daily...

May 15, 2026